Articles by Oakleigh Wealth

Employee Stock Purchase Plans

Employee Stock Purchase Plans give participants the chance to buy company stock at a discount of up to 15% and are funded with regular paycheck withholdings. At the end of the offering period, you can sell the shares and lock in a nearly “risk-free” profit that will be taxed just like a cash bonus, or if you hold the shares, you may become eligible for more favorable capital gains treatment for a portion of the gain (assuming there are gains!)

Restricted Stock Units (RSUs)

RSUs are one of the simplest and most common forms of equity compensation. They are essentially a promise of a given quantity of stock at a future date. Once the shares are vested and taxes are accounted for, you own the company stock just as if you had purchased it on your own. The key question to ask yourself when deciding whether to hold the shares or sell them immediately is this: “If I got a cash bonus instead, would I use it to buy shares in my company?” If not, that’s a good indication that you should just cash out now, or as the Steve Miller Band put it, “Go ahead, take the money and run!”

Tax Prep. vs Tax Planning

To many, this may seem like a distinction without a difference or a trigger for mild nausea and severe eye-glazing! While both are as important as they are interrelated, they are rather distinct in practice.

June 2023 Newsletter: Tax Planning

This month's newsletter is all about taxes!

You're already ahead of the pack if you’ve kept reading beyond the first line. So many individuals try to limit the time and brain space devoted to taxes to the scramble of weeks leading up to Tax Day. The saying about “death and taxes” notwithstanding, there actually is something to be done when it comes to managing the impact and timing of your tax liability over the long run. Still, the time to do something about it is not the first two weeks of April when the bill comes due.

Defining the Elements

At Oakleigh, we use an app called Elements to show a quick snapshot of your financial health and track specific key metrics over time. This is very similar to how a doctor might track your vital signs to understand your physical health and quickly diagnose specific issues. Of course, there’s a story behind all of these numbers and we would dive much deeper for a full financial planning engagement. However, you might be surprised by how many important issues can be uncovered and addressed from these high-level metrics alone.

To Roth or Not to Roth? Deciding Between Roth and Tax-Deferred Savings

The decision of whether to contribute to a Roth or a traditional retirement account basically boils down to timing: do I pay taxes now or later? While both types of retirement accounts are powerful tools for building wealth, this seemingly simple binary can produce some unique planning opportunities with meaningful tax savings for many individuals.

Donor Advised Funds: Don’t be daft, use a DAF

Donor Advised Funds(DAFs) are a simple but powerful tool to facilitate charitable donations, manage tax liabilities, and create a culture or legacy of charitable giving. No one donates to charity just to save on their taxes (the math doesn’t work like that!), and the many personal benefits of charitable giving are not necessarily correlated with the size of your gift or the resultant tax deduction. However, if you are already inclined to give (and I recommend it), DAFs are one of the more effective arrows in the quiver of a financial planner.

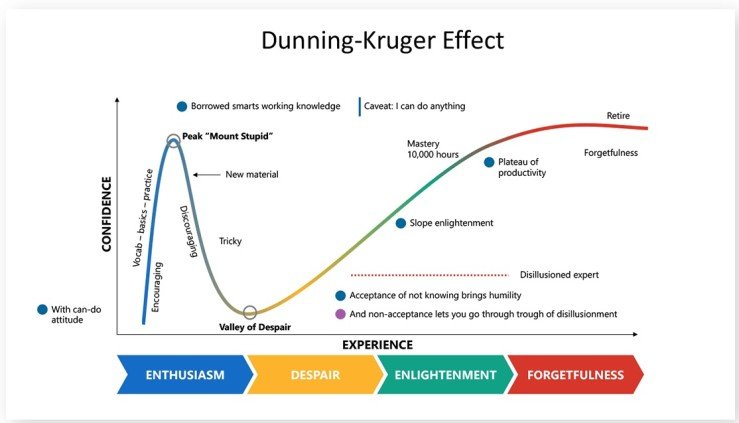

The Dunning-Kruger Effect (in investing (and life)

Dunning & Kruger’s study demonstrated something we all know to be true from experience: people with low levels of knowledge, skill, or competence tend to overestimate their own abilities. Their findings have broad implications for personal finance and investing, but it also raises broader questions about the human experience more generally. We are all prone to over confidence. Mastery, in any arena of life, requires that we overcome the despair of failure through dilligence and humility. But is that all there is?

Financial Assessment for a Couple In their Mid-30s

Ever wondered what a financial assessment looks like? Here’s an example assessment of a married couple in their mid-30s with two young children. Mike is an architect working for a larger firm making $95k per year and his wife Mary just received a raise at the consulting firm she works for, and is now making $260k per year after finishing an executive MBA program. They have two children in daycare, but they feel like they should be able to do more with the good money they’re making now, but life just continues to get more complicated.

8 Things You Should Spend Your Money On

Most of us don’t need any more help perpetuating our arrival fallacies or justifying impulse purchases. Ad agencies, search engines, and Instagram algorithms already have us figured out. Ask my wife, I have no trouble justifying any number of purchases based on how much time they’ll save, what a great investment they are, or how much better off our lives will be once we have ______.

Then there are others whose struggles are in the opposite direction. We all know friends and family members who have plenty of money, but have difficulty spending it, even on things that would really improve their lives, ease some burden, or add a modicum of comfort or enjoyment. “Penny wise, but pound foolish,” as they say..

Whichever camp you fall into, this list of “8 Things You Should Spend your Money On” is for you.

Budgeting is Optional (Tracking is Necessary)

If you’re like me, the idea of budgeting is not very high on your list of things you like to do, falling somewhere between going to the dentist and doing your taxes. If you’ve ever tried co-budgeting with a spouse or partner, it’s at best “no fun,” and at worst it’s an area rife with disagreement, judgment, and defensiveness. You may think you already know where your money is going (you don’t), or perhaps you don’t really want to know… It’s no wonder we don’t do it.

How much should I be saving? Am I on track?

Your savings rate tells an important story about your current financial wellness and preparation for long term financial security. Setting a reasonable savings goal and sticking with it is highly correlated with financial independence. In this article, we'll answer following questions: How much should I be saving? Am I on track? How can I increase my savings rate?

Making Work Optional

This seemingly complicated question can be boiled down to a simple, but powerful metric: your Total term score.

This single number estimates the number of years a person could live on his or her current assets if they did not grow. This includes your cash, investments, business value, and real estate equity. While this key metric is not terribly difficult to calculate, it is powerful in its simplicity and its nuances can lead to very interesting discussions.

A Transparent Look at “Fee-Only” Financial Advising

There are so many different types of “financial advisors” in the marketplace, there’s no wonder that many folks lump them all together into one. Tell someone you’re a financial advisor at a party and they’ll either ask you for your latest stock tip, or they’ll quietly shift their wallet to their front pocket so they can keep an eye on it! In my experience, sadly, the latter is probably the more rational response!

When can I afford to Retire? Part 3: Expenses

Making the transition from building your savings to spending it down can be a jarring one, but arming yourself with knowledge about your actual expenses can give you the confidence to make the transition, which may even be feasible sooner than you think.

Can I Afford to Retire? Part 2: Income

Once you’ve given some thought to what your ideal retirement looks like (see part 1), answering the question “When can I afford to retire?” becomes an exercise in comparing expected future expenses with expected future income over the rest of your life and your spouse’s life. In this second part, we’ll look at the income side of the equation and ask, “where is the money going to come from?”

Can I Afford to Retire (and when)?

“When can I afford to retire?” is the question that drives more individuals into the office of a financial planner than any other. The sooner you start asking it, the better. Too often, the more tangible and immediate concerns of career and family life enable us to put off thinking about retirement, except in the abstract. It seems so far off in the future that it can be difficult to wrap your head around, (that is, until it’s right around the corner!).

In part one of this three-part series, we’ll take a step back and question what will retirement mean for me?

What’s with the name Oakleigh?

When I was 11, my family moved into a neighborhood called Oakleigh Forest, a modest, multi-generational, suburban community near Annapolis, MD made up of hard-working professionals, public servants, and small business owners. It also happened to be the same neighborhood where my father had grown up, and where my newly retired grandparents still resided in that same house down the street.

Term Life Insurance is Probably All You’ll Ever Need

There’s no shortage of life insurance options available, and certainly no shortage of agents eager to sell you any number of policies, but the reality is that basic term life insurance is probably the only type of policy that you really need (and it also happens to be the least complicated and least expensive).